A man with nearly three decades of experience in the car business is revealing how dealerships can secretly mark up your auto loan’s interest rate, potentially adding thousands to your total cost. Zac Smith, who runs the YouTube channel The Car Guy Chronicles With Zac, posted a video breaking down this tactic. The clip went viral on TikTok, attracting over 289,000 views.

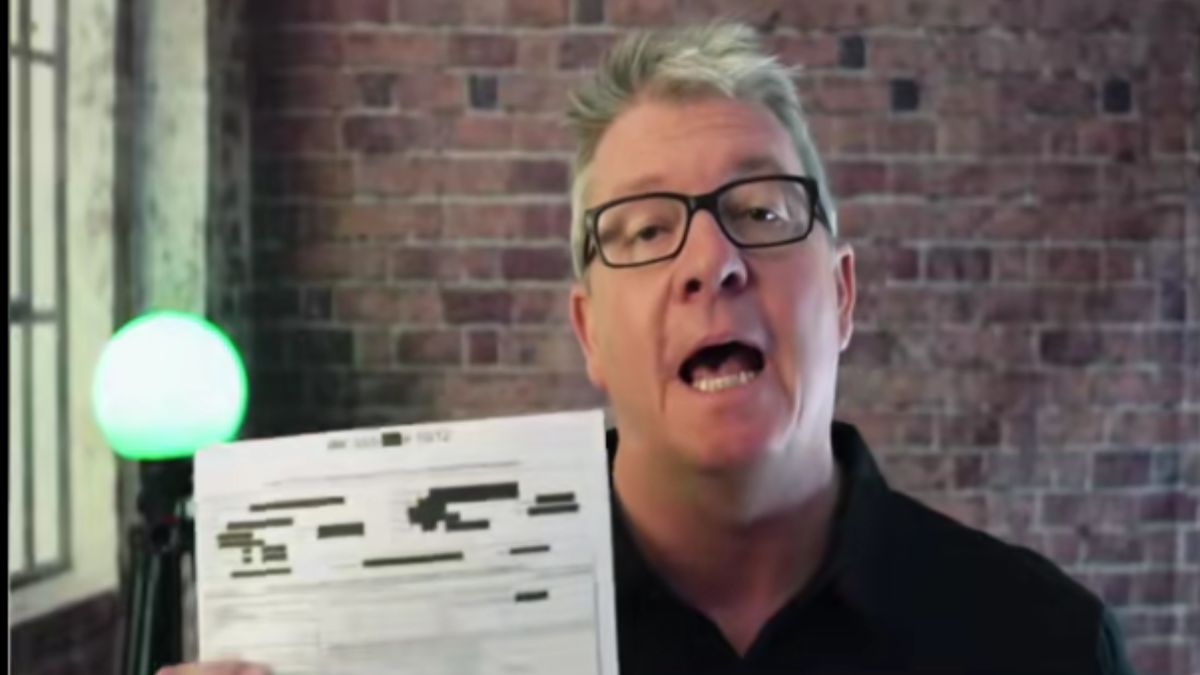

According to Motor1.com, Smith, who admits he used to participate in these practices, showed two documents in his video. “This piece of paper says the bank approved my loan at 8.87%,” he explained, holding up the first. He then displayed the second, stating, “And this is the contract the dealership had me sign at 11.37%. Same day, same bank, same loan.”

“The difference between these two numbers is that the dealership made almost $5,500 in additional profit,” Smith pointed out, confirming he has sat in that finance office manager’s chair and marked up rates himself.

Car loan markups are completely legal, and dealerships are quietly profiting from them

This comes down to what is known as a “buy rate.” When you apply for financing at a dealership, they send your application to multiple banks, sometimes five, ten, or even fifteen. Each bank responds with an interest rate based on your credit, which is your buy rate.

The finance manager then takes that approved rate and can legally add up to 2.5% on top of it. So an 8.87% approval becomes the 11.37% you see on your contract. Smith calls this extra percentage a “kickback,” where the bank pays the markup back to the dealership as a commission, known as “dealer reserve.” Dealerships have several ways of making extra profit off unsuspecting buyers, and loan markups are just one of them.

Smith walked through the numbers to show the real cost. A customer financing $46,869 over 84 months at 8.87% would pay about $750 per month, with total interest of $16,284. At the marked-up 11.37% rate, the monthly payment jumps to $815, pushing total interest to $21,650, a difference of about $5,400, or roughly $66 more per month.

Smith says that is exactly the trick. The monthly increase is small enough that most buyers do not question it, since they are focused on the monthly payment rather than the total loan cost. By the time you reach the finance office, you have usually spent hours negotiating and are ready to leave.

Many people commenting on Smith’s video were not surprised. One commenter wrote, “Reason I always go direct to my bank and get approvals prior to buying a car.” Another shared a personal experience, saying, “This happened to me. My bank told me what they approved me and the dealer marked it up 2%. Great info.” A third commenter mocked, “So you were the bad guy and now decided to be good?”The Consumer Financial Protection Bureau confirms that dealers are not required to offer the best available rate and can legally mark up what they receive from the bank. The best way to protect yourself is to get loan quotes directly from several lenders before visiting a dealership. Some buyers have also found that using a Costco membership to negotiate car deals gives them more leverage against whatever rate the dealership presents.

Published: Mar 16, 2026 01:22 pm